Who Must File a U.S. Tax Return and When a Dual-Status Return Is Required

Many foreign visitors assume that only green card holders or work-visa holders must file U.S. tax returns.

Under U.S. tax law, visa type does not determine tax residency.

Instead, the IRS looks primarily at physical presence in the United States.

Even individuals visiting on a tourist visa may be treated as U.S. tax residents — and in certain years may be required to file a dual-status tax return.

This determination is made under the IRS Substantial Presence Test (SPT).

Official IRS reference: IRS Publication 519, U.S. Tax Guide for Aliens.

Official IRS guidance:

https://www.irs.gov/individuals/international-taxpayers/substantial-presence-test

Who This Article Is For

This guide is especially relevant if you:

- Are living in the U.S. on a tourist or visitor visa

- Are waiting for I-485 or green card approval

- Spend extended time in the U.S. each year

- Earn income outside the United States

- Are unsure whether to file Form 1040, Form 1040-NR, or both

- Are planning to abandon a green card or renounce U.S. citizenship

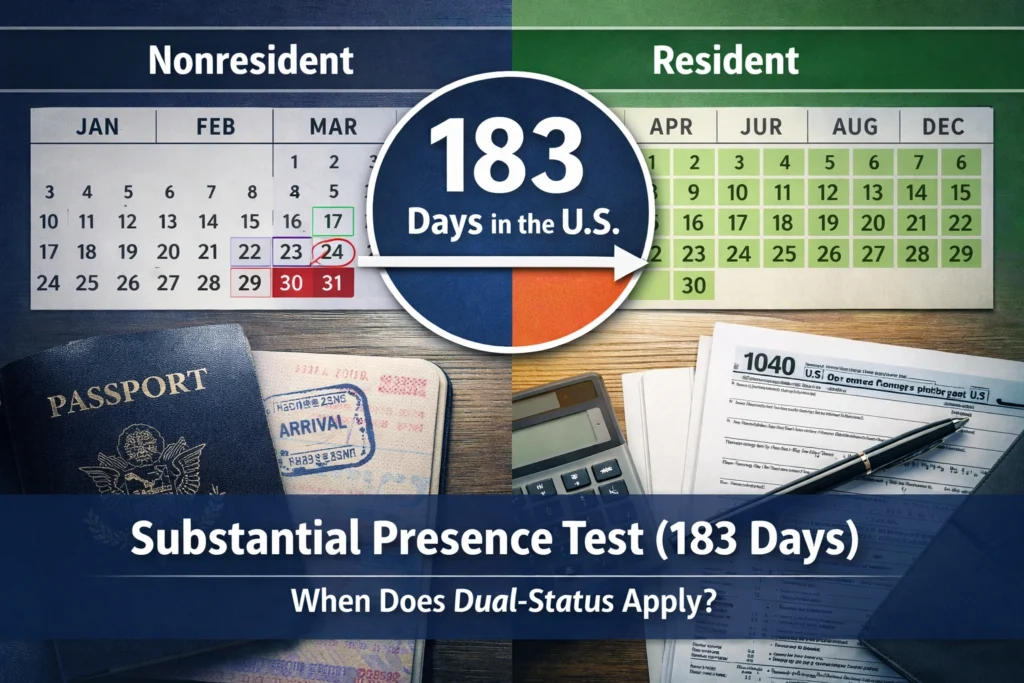

What Is the Substantial Presence Test?

The Substantial Presence Test determines whether a non-U.S. citizen is treated as a U.S. tax resident for a calendar year.

You are considered a U.S. tax resident if both conditions are met:

1️⃣ 31-Day Rule

You were physically present in the United States for at least 31 days during the current year.

2️⃣ 183-Day Weighted Formula

Your total U.S. presence over a three-year period equals 183 days or more, calculated as:

- All days in the current year

- 1/3 of days in the prior year

- 1/6 of days two years ago

If the total equals or exceeds 183 days, you meet the Substantial Presence Test.

Generally, any day physically present counts as a full day, with limited exceptions.

Does Visa Type Matter?

No.

For tax purposes, the IRS does not determine residency based on:

- Tourist vs. work visa

- Immigration intent

- Pending green card status

The IRS looks primarily at days of physical presence.

However, certain visa holders (such as F, J, M, Q students and certain diplomats) may exclude days under special IRS rules — but only if they properly file required forms (such as Form 8843).

What Happens If You Meet the Substantial Presence Test?

If you meet SPT, you are generally treated as a U.S. tax resident.

That typically means:

- Filing Form 1040

- Reporting worldwide income during your period of residency

However, important exceptions may apply:

- Closer Connection Exception (Form 8840)

- Treaty tie-breaker positions (Form 8833)

Residency analysis should always be done carefully before filing.

Foreign Income and Foreign Taxes

If you are treated as a U.S. tax resident, you must report worldwide income — including foreign salary, business income, and investment income.

Double taxation may be reduced through:

- Foreign Tax Credit (Form 1116)

- Applicable tax treaty provisions

But relief depends on:

- Type of income

- Source rules

- Timing

- Credit limitations

Foreign tax paid does not automatically eliminate U.S. tax.

Who May Exclude Days from SPT?

Certain individuals may exclude days of presence, including:

- Diplomats on A or G visas

- Students on F, J, M, Q visas

- Teachers or researchers under limited years

- Individuals unable to leave due to medical condition

- To preserve exclusions, Form 8843 must be filed.

Failure to file Form 8843 may result in the IRS counting those days.

What Is a Dual-Status Tax Year?

A dual-status year occurs when an individual is:

- A nonresident for part of the year, and

- A U.S. tax resident for the remainder of the year

This most commonly occurs in:

- The year of arrival in the U.S.

- The year of departure from the U.S.

When Is a Dual-Status Return Required? (Arrival Year)

Under IRS Publication 519:

If you first meet the Substantial Presence Test during the year,

Your residency generally begins on your first day of physical presence in that year.

This means:

- Before residency start date → Nonresident rules apply

- After residency start date → Resident rules apply

If you are a U.S. resident on the last day of the year, you must:

- File Form 1040 as the main return

- Write “Dual-Status Return” across the top

- Attach Form 1040-NR as a “Dual-Status Statement”

If you are a nonresident at year-end, the structure reverses.

Important Restrictions for Dual-Status Returns

Dual-status taxpayers:

- Cannot claim the standard deduction

- Cannot file jointly (unless making a special election with a U.S. spouse)

- Cannot use Head of Household rates

- Have limited eligibility for certain credits

- Cannot deduct expenses against certain non-effectively connected income

Because of these restrictions, dual-status years often require careful planning.

Dual-Status in an Exit Year

Dual-status may also apply if residency ends during the year, such as:

- Formal green card abandonment

- Renunciation of U.S. citizenship

In that year:

- Resident rules apply before expatriation

- Nonresident rules apply after

Separate expatriation tax rules may also apply depending on net worth and tax history.

Filing Mechanics

If resident at year-end:

- File Form 1040

- Attach Form 1040-NR statement

If nonresident at year-end:

- File Form 1040-NR

- Attach Form 1040 statement

The mechanics are technical and must follow IRS formatting rules.

Additional Elections to Consider

Full-Year Resident Election (Married to U.S. Citizen/Resident)

In limited cases, a dual-status individual married to a U.S. citizen or resident may elect to file jointly and be treated as a full-year resident under IRC §6013.

This may allow:

- Standard deduction

- Joint filing

- Expanded credits

But worldwide income must be included.

Common Filing Errors

We frequently see:

- Assuming visa type controls tax status

- Ignoring worldwide income after meeting SPT

- Filing 1040-NR when 1040 is required

- Filing dual-status when not required

- Missing FBAR reporting

- Failing to analyze residency start date correctly

Key Takeaway

If you meet the Substantial Presence Test, you are generally treated as a U.S. tax resident — regardless of visa type.

Dual-status returns arise only when residency begins or ends during the year.

Because residency status affects:

- Worldwide income reporting

- Deduction eligibility

- Filing forms

- Foreign asset reporting

Careful analysis is critical.

Substantial Presence Test & Dual-Status — Frequently Asked Questions (2025)

Q1. If I am on a tourist visa, do I have to file a U.S. tax return?

Possibly. Visa type does not determine tax residency. If you meet the Substantial Presence Test (SPT), you may be treated as a U.S. tax resident and required to file Form 1040.

Q2. Does a pending I-485 automatically make me a U.S. tax resident?

No. Immigration status and tax residency are separate systems. Tax residency is determined primarily by physical presence under the Substantial Presence Test.

Q3. If I entered the U.S. mid-year and stayed, am I automatically dual-status?

Often, yes. If you first meet the Substantial Presence Test during the year, residency generally begins on your first day of presence, which can create a dual-status tax year.

Q4. What is the difference between Form 1040 and Form 1040-NR?

Form 1040 is filed by U.S. tax residents. Form 1040-NR is filed by nonresident aliens. In a dual-status year, both forms may be used — one as the main return and the other as a supporting statement.

Q5. If I meet the Substantial Presence Test, must I report foreign income?

Yes. Once you are treated as a U.S. tax resident, you must report worldwide income during your residency period.

Q6. Will I be taxed twice on my foreign income?

Not necessarily. The Foreign Tax Credit (Form 1116) may reduce or eliminate double taxation, depending on income type and foreign tax paid.

Q7. Is income earned before moving to the U.S. taxable?

It depends on your residency start date. Income earned before becoming a U.S. tax resident is generally treated under nonresident rules.

Q8. Can I claim the standard deduction in a dual-status year?

Generally no. Dual-status taxpayers cannot claim the standard deduction unless a special election applies.

Q9. Can I file jointly with my spouse in a dual-status year?

Normally no. However, if married to a U.S. citizen or resident, you may elect to file jointly and be treated as a full-year resident under IRC §6013.

Q10. What happens if I meet SPT but do not file?

Failure to file when required can result in penalties, interest, and possible complications in future immigration matters.

Q11. What is the Closer Connection Exception?

If you meet SPT but maintain a closer connection to another country, you may qualify to file Form 8840 and remain a nonresident — if eligibility requirements are met.

Q12. Do I need to file FBAR if I become a U.S. tax resident?

Possibly. If your foreign financial accounts exceed $10,000 in aggregate at any time during the year, FBAR (FinCEN Form 114) may be required.

Q13. What if I do not have a Social Security Number?

You may need to apply for an ITIN by filing Form W-7 together with your tax return.

Q14. Can I choose to be treated as a full-year resident instead of dual-status?

Only in limited circumstances — typically if you are married to a U.S. citizen or resident and make a joint election.

Q15. When should I consult a CPA regarding SPT or dual-status?

You should seek professional advice if you arrived mid-year, have foreign income or assets, plan to abandon a green card, or are unsure of your residency classification.

Disclaimer

This article is for educational purposes only and does not constitute tax advice.

U.S. tax residency and filing obligations depend on specific facts and circumstances.

Consult a qualified CPA for advice tailored to your situation.